The earthquake that occurred in Japan in March this year is impacting the production of Toshiba and Sony's CMOS image sensors. Toshiba's Iwate image sensor factory has been shut down. It produces logic chips and CMOS image sensors for mobile phone cameras. Similarly, Sony's CMOS image sensors for mobile phone OEMs have also delayed shipments.

The earthquake that occurred in Japan in March this year is impacting the production of Toshiba and Sony's CMOS image sensors. Toshiba's Iwate image sensor factory has been shut down. It produces logic chips and CMOS image sensors for mobile phone cameras. Similarly, Sony's CMOS image sensors for mobile phone OEMs have also delayed shipments. Pamela Tufegdzic, a consumer electronics analyst at IHS iSuppli, said: “Toshiba is the fifth largest supplier of mobile phone image sensors in the world in 2010, accounting for 13.1% of global sales. Sony ranked sixth, with a market share of 3.9%. The company together accounted for 17% of the global mobile phone digital camera image sensor sales."

Although the production and distribution of CMOS image sensors are affected, the supply of CCD, another major image sensor technology, seems to be unaffected, at least in the short term. Japanese suppliers such as Sony, Panasonic, Fujifilm, Sharp and Toshiba control the global CCD market.

Due to the higher image quality, CCDs are commonly used in digital cameras. On the contrary, lower-cost CMOS sensors are mainly used in mobile phones and other products. For these products, shooting is a secondary function.

Hua Jing and Canon Enterprises are Taiwan's digital camera manufacturers and OEM for major Japanese brands. The two companies stated that there has been no shortage of CCD image sensor supplies from Japan in the near future. Canon's 90% of CCD devices come from Sony, and Huajing's 70-80% of CCD devices come from Sharp. Sharp's Japan CCD factory is far from the hardest hit, and Sony's CDD factory is located in Thailand.

Therefore, CCD supply should not be a problem in the short term. However, in the long term, the situation may change because the upstream material supply of the CCD manufacturer may be in a situation where it may face transportation and power problems.

Due to the impact of the earthquake, Japanese digital camera brands such as Panasonic, Canon and Nikon were forced to close some of the high-end production lines of digital cameras in Japan. These companies pointed out that since their low-end consumer models are mainly produced in factories in China and Thailand, or outsourced to Taiwanese companies, it is not expected that the earthquake will have a serious impact on these products.

The earthquake in Japan also led to a 1.1% reduction in global DRAM shipments in March and April. This, together with other factors, helped stabilize the contract price of DRAM in March. March is usually weak for DRAM, and the price will drop by about 3%. The current price stability in March is of great significance. It will greatly enhance the annual DRAM sales.

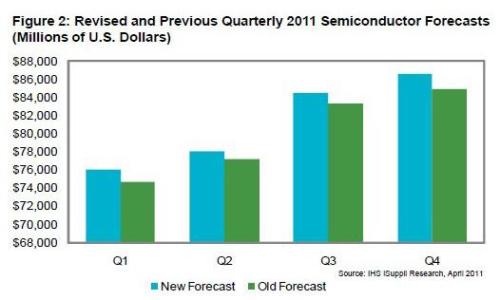

Each quarter of 2011, semiconductor sales will be higher than previous estimates, as shown above.

The average contract price for DRAM in April is expected to rise from flat to 2%, while the previous forecast is a 3-4% drop.

Japan's two DRAM factories were not damaged in this earthquake. However, Elpida’s production at a chip assembly plant in the Akita region was interrupted, causing shipments to decline.

If Japan recovers quickly, it is expected that the pressure of rising DRAM prices will weaken in the second half of this year. However, if the shortage of wafers deteriorates, DRAM prices may rise further later this year.

Japan is the world's major producer of silicon wafers, accounting for 60% of global supply. Silicon wafers are a key raw material for the production of semiconductors. The major wafer supplier Shin-Etsu's 300-mm wafer production is still not normal. The company's Shenji and Baihe plants are closed, and the two plants together account for about 20% of global wafer production.

Therefore, the supply of 300mm bare wafers may become a problem for memory manufacturers. If the supply problem cannot be solved in the short term, the production efficiency will be affected after the bare wafer inventory is depleted. In particular, DRAM production will be affected when the number of wafers in the manufacturing supply chain drops to less than 50% of the normal level.

Mike Howard, chief DRAM analyst at IHS iSuppli, said: "From the beginning of October will face this possibility, leading to further rise in DRAM prices."

12 Woofer Speaker,Woofer Speaker 12 Inch,12 Inch Woofer Speaker,Pro Audio Tweeter Speaker

Guangzhou Yuehang Audio Technology Co., Ltd , https://www.yhspeakers.com